$5108 Social Security Payments in 2025: Social Security plays a crucial role in retirement planning, offering financial stability to millions of Americans. But did you know that you could receive up to $5,108 per month in Social Security payments if you retire at age 70? This article will break down how you can qualify for this maximum benefit, explain the key factors that affect your Social Security payments, and provide actionable advice to help you optimize your retirement income. Understanding these factors is essential for making informed decisions about your future.

$5108 Social Security Payments in 2025

| Key Insights | Details |

|---|---|

| Maximum Monthly Benefit (2025) | $5,108 for retirees claiming benefits at age 70. |

| Requirements | 35 years of earnings, maximum taxable income, and delaying benefits until 70. |

| Earnings Cap (2025) | Maximum taxable earnings set at $176,100. |

| Official Source | Social Security Administration |

| Practical Tips | Work longer, increase earnings, and delay claiming benefits. |

Qualifying for the $5,108 maximum Social Security payment requires careful planning, consistent high earnings, and a strategic approach to claiming benefits. Even if you don’t qualify for the maximum, implementing strategies like working longer, increasing your income, and delaying benefits can significantly enhance your retirement income. Understanding the impact of COLA and coordinating with a spouse can further boost your financial security.

USA $5,108 Maximum Benefit

The $5,108 monthly benefit is the highest Social Security retirement payment for 2025. Achieving this amount requires meeting specific criteria over your working life. Here’s what you need to know to set yourself up for success:

1. Work 35 Years or More

Your Social Security benefit is calculated based on your highest 35 years of earnings. If you worked fewer than 35 years, the SSA averages in zeros, which can significantly reduce your payment. This emphasizes the importance of maintaining steady, long-term employment to secure a robust retirement benefit.

2. Earn the Maximum Taxable Income

The maximum taxable earnings limit for Social Security is updated annually. In 2025, this cap is $176,100. To qualify for the maximum benefit, you need to have earned at or above this limit for 35 years. This requires sustained career growth, promotions, and leveraging opportunities to maximize earnings over time.

3. Delay Benefits Until Age 70

Although you can claim benefits as early as age 62, delaying until age 70 maximizes your monthly payments. For each year you delay past your full retirement age (FRA), your benefits increase by 8% due to delayed retirement credits. This strategic delay can significantly enhance your financial security in later years.

How to Calculate Your Social Security Payments?

To estimate your Social Security benefits, follow these steps:

Step 1: Review Your Earnings Record

Log in to your My Social Security account on the SSA website to review your earnings history. Ensure all your earnings are accurately reported. Errors or omissions can lead to lower payments, so it’s crucial to address discrepancies early.

Step 2: Use the SSA’s Benefit Calculators

The SSA provides tools like the Retirement Estimator and the Detailed Calculator to help you project your benefits based on your work history and expected retirement age. These calculators are user-friendly and allow you to experiment with different scenarios, such as retiring early or delaying benefits.

Step 3: Factor in Delayed Retirement Credits

If your FRA is 67 and you wait until 70 to claim benefits, your monthly payments increase by 24% (8% per year for three years). This significant boost can make a substantial difference in your overall retirement income, especially if you expect to live longer.

Strategies to Boost Your Social Security Benefits

Even if you can’t reach the maximum payment, there are practical ways to increase your monthly benefits:

1. Work Longer

Every additional year of work can replace a lower-earning year in your 35-year average, boosting your benefit. Extending your career even by a few years can have a positive impact on your financial future.

2. Increase Your Earnings

Aim to maximize your annual income, especially during your highest-earning years. Consider side hustles, promotions, or job changes to achieve higher earnings. For example, taking on leadership roles or acquiring certifications can lead to substantial salary increases.

3. Delay Claiming Benefits

If financially feasible, delay claiming Social Security until 70. This strategy can significantly enhance your monthly payments and provide greater financial security during retirement.

4. Coordinate with a Spouse

Couples can use strategies like file-and-suspend or claim spousal benefits to optimize their combined Social Security income. Spousal benefits can provide up to 50% of the higher-earning spouse’s FRA benefit, adding an extra layer of financial stability.

Real-Life Example: How Delaying Benefits Pays Off?

Let’s consider an example:

- John’s FRA: 67, with an estimated monthly benefit of $3,500.

- If John claims at 62: His benefit is reduced by 30%, giving him $2,450 per month.

- If John claims at 70: His benefit increases by 24%, providing $4,340 per month.

By waiting until 70, John receives nearly $1,900 more per month compared to claiming at 62. Over a 20-year retirement, this decision could result in an additional $456,000 in total benefits, demonstrating the power of delayed claiming.

The Impact of COLA on Your Benefits

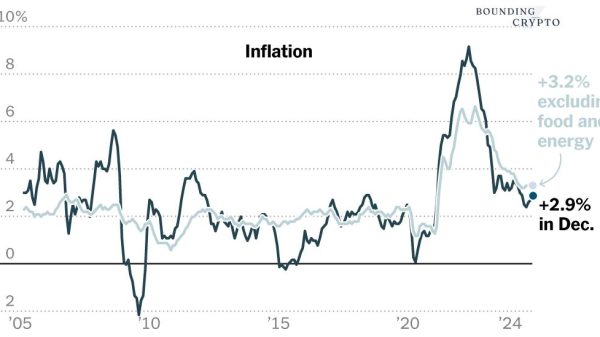

The Cost-of-Living Adjustment (COLA) is another critical factor in maximizing your Social Security benefits. COLA ensures that your payments keep pace with inflation. For example, a 3.2% COLA in 2025 would increase a $4,000 monthly benefit by $128, providing additional financial security as living costs rise.

COLA Boost in 2025: Are You Last to Get Paid in January! Check Here

$600 Social Security for these Recipients, Thanks to COLA— Check Payment Date & Eligibility

Ensure Your COLA Increase Today: What Every Retiree Needs to Know!

Frequently Asked Questions (FAQs)

1. Who qualifies for the maximum Social Security benefit?

To qualify, you need:

- At least 35 years of earnings at or above the annual taxable maximum.

- To delay claiming benefits until age 70.

2. What is the full retirement age (FRA)?

FRA varies based on your birth year. For those born in 1960 or later, FRA is 67. Check the SSA’s FRA chart for details.

3. Can I receive Social Security while still working?

Yes, but if you claim benefits before FRA, your payments may be reduced if your earnings exceed the annual limit ($21,240 in 2025). Once you reach FRA, earnings no longer affect your benefits.

4. Are Social Security benefits taxable?

Depending on your income, up to 85% of your benefits may be taxable. Learn more on the IRS website.

5. How does COLA affect Social Security payments?

The Cost-of-Living Adjustment (COLA) ensures benefits keep pace with inflation. For 2025, the COLA is expected to be around 3.2%. This adjustment helps retirees maintain their purchasing power over time