$3,089 for these Senior couples in Social Security in 48 hours: Social Security is a vital lifeline for many seniors in the United States. In just 48 hours, senior couples across the country will receive an average of $3,089 in Social Security benefits. This increase comes as part of the annual Cost-of-Living Adjustment (COLA), designed to help beneficiaries keep up with inflation. But are you eligible for this payment, and how can you maximize your benefits? Let’s break it down.

$3,089 for these Senior couples in Social Security in 48 hours

| Aspect | Details |

|---|---|

| Average Monthly Benefit | $3,089 for senior couples |

| COLA Increase | 2.5% in 2025 |

| Maximum Individual Benefit | $5,108 per month (for those delaying retirement to age 70) |

| Eligibility Factors | Based on earnings record, work history, and retirement age |

| Payment Start Date | Payments will begin in January 2025 |

| Official Resources | Visit the Social Security Administration (SSA) for more information |

The $3,089 Social Security payment for senior couples in 2025 is a reflection of the Social Security Administration’s efforts to support retirees amid rising living costs. Understanding eligibility requirements and implementing strategies to maximize benefits can ensure financial stability during retirement. Whether you’re planning to claim benefits soon or looking to optimize your retirement income, knowledge is your greatest asset.

Taking proactive steps, such as delaying retirement, reviewing your earnings record, and coordinating with your spouse, can significantly increase your benefits and improve your financial security. With proper planning and informed decisions, you can make the most of the Social Security benefits available to you.

What Is the Cost-of-Living Adjustment (COLA)?

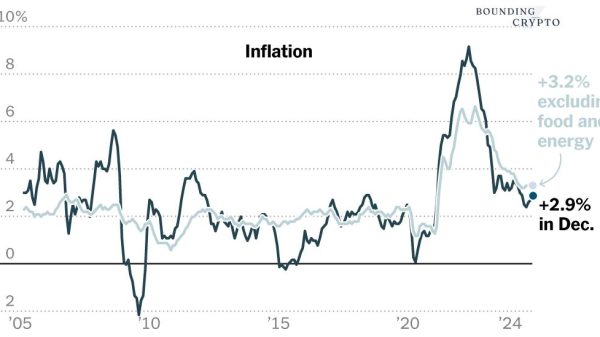

The Cost-of-Living Adjustment (COLA) is an annual increase in Social Security benefits designed to counteract inflation. It ensures that beneficiaries maintain their purchasing power as the cost of goods and services rises. For 2025, the COLA is set at 2.5%, which translates into higher monthly payments for all recipients.

For senior couples, this means an average monthly benefit of $3,089, up from $3,014 in 2024. This adjustment reflects the Social Security Administration’s commitment to supporting retirees in an ever-changing economic landscape.

The COLA is determined by changes in the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). If inflation rises, COLA increases ensure that beneficiaries’ purchasing power remains steady. This year’s 2.5% adjustment accounts for moderate inflation trends, reflecting the federal government’s data-driven approach to protecting seniors’ financial security.

Are You Eligible for $3,089?

Your eligibility for Social Security payments depends on several factors:

1. Work History

Social Security benefits are based on your 35 highest-earning years. If you or your spouse worked fewer than 35 years, zeros are factored into the calculation, potentially reducing your benefits. It’s important to maximize your earnings during your career to qualify for higher benefits. For individuals who had part-time work or extended career breaks, working additional years to replace zero-income years can significantly increase future payouts.

2. Earnings Record

The higher your lifetime earnings, the higher your benefits. For example, individuals who earned at or above the taxable maximum for at least 35 years may qualify for the maximum monthly benefit of $5,108 (if they delay retirement until age 70). Lower earners can still increase their benefits by taking advantage of spousal or delayed retirement credits.

3. Retirement Age

Your Full Retirement Age (FRA) is based on your birth year. For those born in 1960 or later, the FRA is 67. Claiming benefits before reaching FRA results in reduced monthly payments, while delaying benefits beyond FRA increases them. For instance, claiming benefits at age 62 can reduce payments by as much as 30%, while waiting until age 70 can boost them by 24% or more. Calculating the tradeoffs based on your financial situation is crucial.

4. Spousal Benefits

If one spouse had lower earnings or didn’t work, they might qualify for spousal benefits, which can be up to 50% of the higher-earning spouse’s benefit. This can significantly boost household income, particularly for single-income households. Spouses should carefully plan the timing of their claims to maximize their combined benefits over time.

How to Maximize Your Social Security Benefits

To make the most of your Social Security income, consider the following strategies:

1. Delay Retirement

Delaying your benefits beyond your FRA increases your monthly payment by approximately 8% per year until age 70. For example, if your FRA is 67, waiting until 70 can result in a significantly higher benefit. This strategy is especially effective for individuals in good health with a longer life expectancy, as they stand to collect more over their lifetimes.

2. Work for At Least 35 Years

Ensure you have 35 years of earnings to avoid zeros being factored into your calculation. If you’ve worked fewer than 35 years, consider working additional years to replace low- or zero-earning years. Even part-time work late in your career can improve your earnings record and increase your benefit amount.

3. Maximize Your Earnings

Aim to earn at or above the taxable wage base, which for 2025 is $176,200. High lifetime earnings directly translate into higher benefits. If you’re in your peak earning years, contribute as much as possible to retirement accounts, and focus on advancing in your career or taking on additional work opportunities to enhance your earnings.

4. Coordinate With Your Spouse

Strategize with your spouse to determine the best time for each of you to claim benefits. For instance, one spouse may claim earlier while the other delays benefits to maximize the household’s income. This approach can be particularly helpful for couples with disparate earnings histories, as it allows you to optimize the timing and amount of your combined benefits.

5. Review Your Social Security Statement

Regularly reviewing your Social Security statement ensures that your earnings record is accurate. Mistakes in reporting can lower your benefits, so it’s important to verify the data and report any errors to the SSA promptly. You can access your statement online through your My Social Security account.

When Will You Receive Your $3,089 Payment?

Social Security payments are distributed based on your date of birth. Here’s the schedule for January 2025:

- January 8: Beneficiaries born on the 1st–10th of any month.

- January 15: Beneficiaries born on the 11th–20th.

- January 22: Beneficiaries born on the 21st–31st.

If you’ve been receiving benefits since before May 1997 or if you receive Supplemental Security Income (SSI), your payment will be issued on January 3. Ensure that your direct deposit information is up to date to avoid delays in receiving your benefits.

Additionally, for those who rely on mailed checks, remember that postal delays can occasionally affect delivery times. Setting up direct deposit is the most secure and timely method for receiving your benefits.

No More $1907 Social Security Checks in 2025 – See If You’re on the List!

$292 Monthly SNAP Payments Per Person: Will you get it? Check Eligibility

Surprise Boost for SSI Recipients: What the 2025 Adjustments Mean for You?

Ensure Your COLA Increase Today: What Every Retiree Needs to Know!

Frequently Asked Questions (FAQs)

Q: What is the Full Retirement Age (FRA)?

A: The FRA is the age at which you qualify for full Social Security benefits without reductions. For individuals born in 1960 or later, the FRA is 67.

Q: Can I receive Social Security benefits if I’m still working?

A: Yes, but if you’re below your FRA, your benefits may be temporarily reduced based on your earnings. Once you reach FRA, there’s no penalty for working while collecting benefits.

Q: How is COLA determined?

A: COLA is based on changes in the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). This ensures benefits keep pace with inflation and adjust annually to reflect changes in living costs.

Q: Can both spouses receive Social Security benefits?

A: Yes. Both spouses can receive benefits based on their individual earnings records. Additionally, spousal benefits may be available for the lower-earning spouse.

Q: What happens if I claim benefits before my FRA?

A: Claiming before FRA reduces your monthly payment. For instance, claiming at age 62 could reduce your benefit by up to 30%. However, if you need the income, claiming early can still be a viable option.

Q: Are Social Security benefits taxed?

A: Yes, depending on your total income, up to 85% of your Social Security benefits may be subject to federal taxes. Some states also tax Social Security benefits, so it’s important to understand the tax implications in your area.